The new lease accounting standard will bring significant change to processes and systems. Experience shows that respective projects are underestimated, and that the ideal tool support is difficult to find.

A Progress Report

IFRS16 – What’s the change?

In early 2016 the International Accounting Standards Board (IASB) issued ‘IFRS 16 Leases’. It sets out principles for the recognition, measurement, presentation and disclosure of leases for both the lessee and the lessor.

In IAS 17 a lease had to be classified by the lessee as either finance lease or operating lease. When a lease was identified as being economically similar to a purchase of the asset, this lease was classified as a finance lease and had to be reported on the balance sheet. All other leases were treated as operational leases and not shown on the balance sheet (‘off-balance-sheet-leases’).

This changes rapidly with IFRS16. Instead of the distinction of operating and finance leases, all leases that exceed certain thresholds with regards to contract durations and lease values have to be reported on the balance sheet.

When IFRS16 becomes effective on 1st January 2019, a lessee will need to …

- capitalize the right to use the underlying asset (‘Right of Use ROU’)

- recognize the financial liability representing the obligation for future lease payments

- separate the depreciation part of the lease assets from interest on lease liabilities in the income statement

… for all contracts that are to be considered leasing contracts.

Implementation projects are often badly underestimated

According to a Lease Accounting Report in Februar 2017 with over 250 accounting and finance leaders, around 70% of the participants had not yet started an operational IFRS16 project until then. It seems many companies underestimated the complexity of such projects. To our experience, implementation projects are heavily underestimated in many companies.

- The complexity of the own leasing business is underestimated, as today most leasing contracts are intransparent to central financial management.

- The complexity to define totally new leasing processes is underestimated. For example, a respective integration to financial systems is typically required. But an integration might also be relevant for contract management solutions, approval workflows, purchasing etc. If this is not taken into account, the lease management will become another isolated system, causing high future total cost of ownership.

- The problem of data gathering of existing contracts is underestimated. Depending on the transition method, this task can become a major and time-critical challenge.

IFRS16 – Why many tools are no perfect fit

It is not exaggerated to state that most existing ERP-systems are not prepared to support the administration of leasing contracts very well. The problem is not to book assets, liabilities, interest and depreciation, but to administrate the contract details throughout their lifecycle. A suitable system should support the full spectrum of lease management in one central solution.

Currently a number of tools are coming up that can calculate the numbers and accounts that need to be booked for leasing contracts. These tools, mainly originating from an EPM background, are not ideally suited to support complex organizations in their lease administration, as they only fulfill parts of the requirements. They are typically able to administrate leasing contracts and to do the necessary calculations (NPV, IRR etc.), but they are not integrated with the ERP-systems that hold relevant master data and that need to receive final bookings.

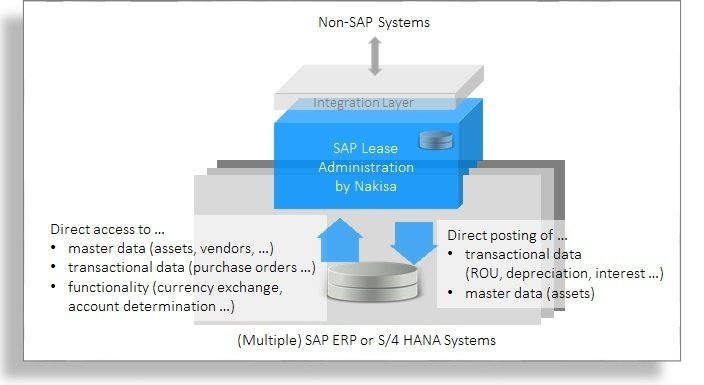

An ideal solution, however, should neither be an isolated lease administration tool nor a pure booking extension to a finance tool. Instead, it should work like a distinct “subledger” for leasing contracts, which combines special lease administration functionality with a direct ERP-integration. As companies can have several ERP-systems from different vendors in their architecture, the central lease administration tool needs to be able to connect different organizational units to different systems. A separate tool is therefore preferable compared to a solution within one of the existing ERP systems.

Our Point-of-View-Paper on IFRS16 discusses in detail the requirements which a suitable solution needs to fulfill. It also shows one solution which integrates seemlessly into SAP ERP systems and which at the same time can work as a standalone lease administration system: SAP Lease Administration by Nakisa.

You are interested in more project-related PoV-Papers? You might want to read about our consolidation solutions with BPC Embedded, our project at Orell Füssli or our BPC solution for a chemicals company.

By Andreas Krüger